Credit Freeze in 2026: Lock My Credit in 15 Minutes

Last updated: 2026-07-01.

A credit freeze is the single most effective identity-theft defense you can deploy in 15 minutes — and federal law makes it free at every major bureau, for every U.S. consumer.

TL;DR: A credit freeze locks your credit report so no lender can pull it without your PIN. That alone stops the most common form of identity theft: new-account fraud. Freeze your credit at Equifax, Experian, and TransUnion (each takes about five minutes), then request your free LexisNexis Consumer Disclosure Report — a separate file that insurers, landlords, and employers pull on you. If you have kids, freeze their credit too. Total time: ~15 minutes. Total cost: $0.

The urgency has climbed sharply in 2026. Javelin Strategy & Research’s 2026 Identity Fraud Study, released in April 2026, found that new-account fraud — the exact attack a credit freeze stops — surged 31% in 2025 to 5.4 million victims and $7 billion in losses, the only fraud category that grew year over year while others fell. Most people know about the three credit bureaus — Equifax, Experian, and TransUnion. Very few know they can flip a switch that essentially turns off new-account fraud for free. Fewer still know that LexisNexis maintains a separate consumer file on nearly every U.S. adult, and that insurance companies, landlords, and employers use it to make decisions about you long before you ever sign a lease or get a quote.

This guide walks through every step of freezing your credit at all three bureaus, requesting your LexisNexis report, freezing your kids’ credit, and what I personally learned after freezing (and thawing) my own credit multiple times over the past several years.

Jump to a section:

- What is a credit freeze, exactly?

- How do I freeze my credit at Equifax, Experian, and TransUnion?

- Does a credit freeze affect my credit score?

- What does a LexisNexis report show, and how do I get mine?

- How do I freeze my child’s credit report?

- What did I learn from freezing (and thawing) my own credit?

- Should I lock my credit right now?

What is a credit freeze, exactly?

Direct answer: A credit freeze is a free federal protection that blocks lenders from pulling your credit report. Without a credit pull, new-account applications are denied on the spot — even if a thief has your full Social Security number.

A credit freeze (sometimes called a “security freeze”) is a request to each of the three major credit bureaus to restrict access to your credit file. When a lender, credit card issuer, or apartment complex tries to pull your credit, the request is blocked until you temporarily lift the freeze with a PIN or password.

The Federal Trade Commission’s guidance on credit freezes and fraud alerts describes a freeze as a way to restrict access to your credit report so identity thieves can’t open new accounts in your name. Per the FTC’s IdentityTheft.gov contacts page, every U.S. consumer has the right to place, lift, and remove a credit freeze for free under the Economic Growth, Regulatory Relief, and Consumer Protection Act (Public Law 115-174), which amended the Fair Credit Reporting Act to require free nationwide credit freezes.

A credit freeze stops the most common identity-theft attack pattern in the United States: new-account fraud. According to the FTC’s 2024 Consumer Sentinel Network Data Book, credit-card fraud was again the #1 type of identity theft reported — 449,032 complaints in 2024, up 7.8% year over year, and nearly 9 in 10 of those involved someone using a victim’s stolen information to open a brand-new credit card. A freeze closes that door before the thief can even knock.

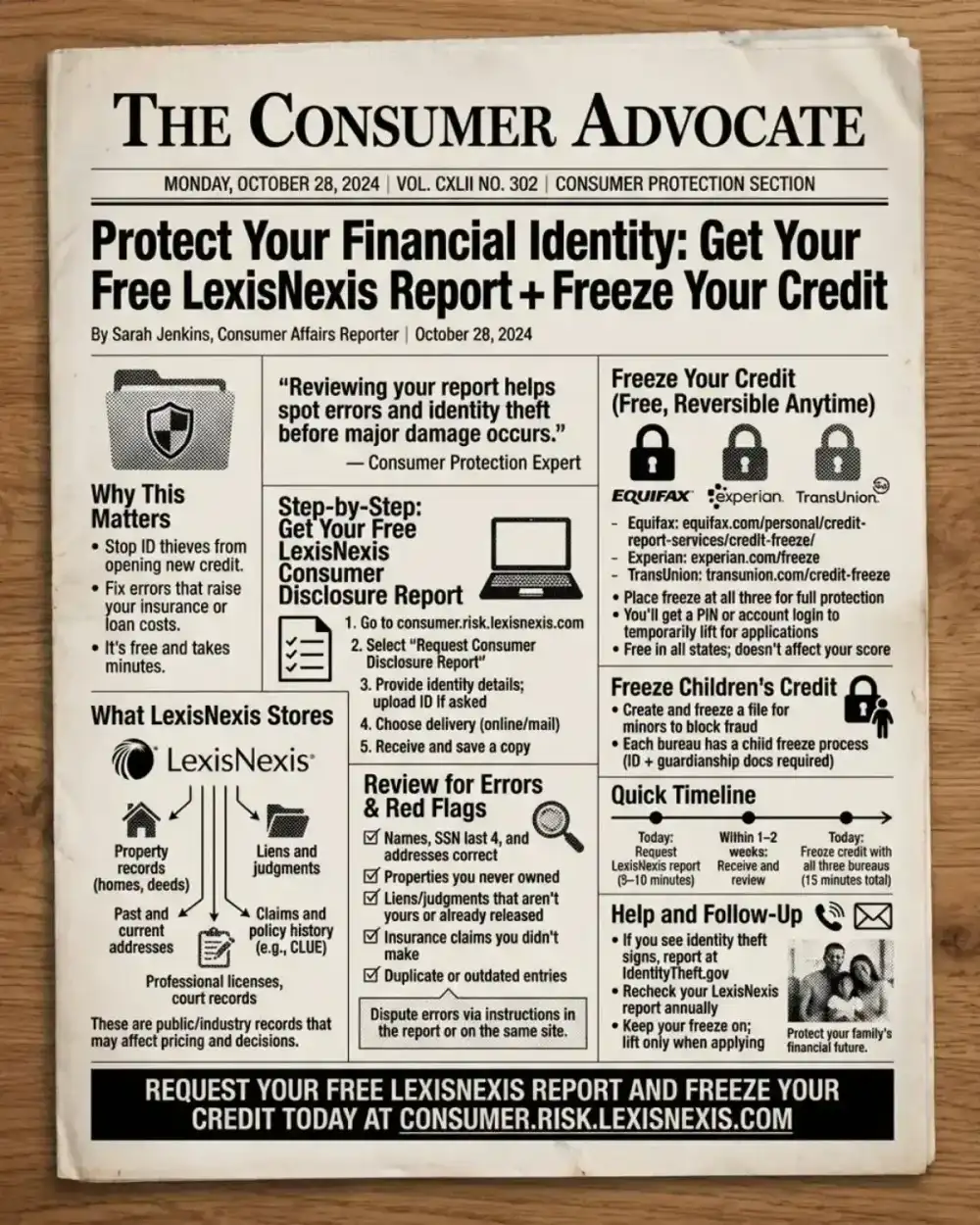

How do I freeze my credit at Equifax, Experian, and TransUnion?

Direct answer: Visit each bureau’s freeze page, create an account, verify your identity, and place the freeze. Equifax, Experian, and TransUnion credit freezes each take about five minutes online — and you must do all three, because lenders check different bureaus.

You have to freeze your credit at each bureau separately. Lenders use different bureaus for different decisions, so a freeze at only one is like locking the front door and leaving the back two wide open. Plan for ~15 minutes total, ideally with your password manager open and a notepad handy for confirmation numbers.

Equifax credit freeze

Go to Equifax’s security freeze page and click “Place a Freeze.” Create a myEquifax account if you don’t already have one. Equifax will verify your identity with knowledge-based questions (prior addresses, old loan balances). Once approved, the Equifax credit freeze is instant — and you’ll get a confirmation email. Save that email and store any PIN they provide in a password manager.

Experian credit freeze

Go to Experian’s freeze center. Experian requires you to create an account, then walks you through identity verification. The Experian credit freeze takes effect immediately. Experian still issues a PIN you’ll need to lift the freeze later — store it in 1Password, Bitwarden, or whichever password manager you trust, not a sticky note. If you lose the PIN, Experian’s recovery process is the slowest of the three (more on that in the lessons section).

TransUnion credit freeze

Go to TransUnion’s freeze portal and follow the same flow. The TransUnion credit freeze is the fastest of the three in my experience — TransUnion defaults to a username/password rather than a numeric PIN, which I find easier to manage long-term. Save the credentials in your password manager.

After all three freezes are in place, freeze credit report access is locked at every major bureau. Each one sends a confirmation. Keep them.

What about Innovis and ChexSystems?

Two smaller bureaus also keep files that some lenders and banks check:

- Innovis is sometimes called the “fourth” credit bureau, used by some lenders for fraud screening and pre-screened offers.

- ChexSystems is used by banks to decide whether to open a new checking or savings account.

Both offer free security freezes. If you’re being thorough, freeze these too. Total additional time: about 10 minutes.

Does a credit freeze affect my credit score?

Direct answer: No. A credit freeze does not affect your credit score. Existing credit cards, loans, and accounts work normally. A freeze only blocks new credit inquiries, so new lenders can’t pull your file until you thaw it.

A common misconception is that freezing your credit will tank your score, or cause your existing accounts to act strange. Neither is true. Your existing credit cards, mortgage, auto loans, and student loans all continue to function exactly as they did before. Your credit score is calculated from the contents of your credit report, not from how often it gets accessed.

What changes is that new applications for credit get denied at the inquiry stage. If you apply for a new card or loan yourself, you’ll need to temporarily “thaw” your file at whichever bureau the lender uses — usually for a single event or a window of a few days. Thawing is online, free, and takes under a minute at each bureau. There’s no penalty for freezing and thawing repeatedly.

This also means a credit freeze is reversible. If you ever decide you don’t want one, you can remove the freeze permanently in the same place you placed it. It’s not a one-way door.

A freeze is also stronger than a credit monitoring service alone. Products like LifeLock, Aura, IDShield, and Experian IdentityWorks alert you after a thief uses your information. A freeze prevents the misuse in the first place. Use monitoring as a tripwire on top of the freeze, not as a substitute for it — and pull your three free annual credit reports at AnnualCreditReport.com, the only federally authorized source under the FCRA.

What does a LexisNexis report show, and how do I get mine?

Direct answer: Your LexisNexis Consumer Disclosure Report is a separate dossier insurers, landlords, and employers buy on you — address history, property records, liens, judgments, licenses, and bankruptcies. Request it free at consumer.risk.lexisnexis.com or 1-866-897-8126.

LexisNexis Risk Solutions is one of the largest data brokers in the world — and most consumers don’t know they have a file with them. Unlike a credit report (which lenders pull), the LexisNexis file is what insurance underwriters, employer background-check companies, landlords, and some financial institutions pull when they’re making decisions about you.

Under the Fair Credit Reporting Act (FCRA), you have the right to request a free copy of your file. There are three ways to do it:

- Online: Submit a request through the official LexisNexis Consumer Portal. After identity verification, you’ll receive a letter via U.S. Mail with instructions to access your report online. Expect 7–14 days end-to-end.

- By mail: Download and complete the Printable Request Form from the portal and mail it to: LexisNexis Risk Solutions Consumer Center P.O. Box 105108 Atlanta, GA 30348-5108

- By phone: Call 1-866-897-8126 and request your free consumer disclosure.

What to look for in your LexisNexis report

When the report arrives, comb through it for:

- Addresses you’ve never lived at

- Property transactions you didn’t make

- Liens or judgments you don’t recognize

- Professional licenses that don’t belong to you

- Bankruptcies, traffic violations, or court records that aren’t yours

If you find errors, dispute them directly with LexisNexis through the same consumer portal. Inaccurate information in their system may be quietly raising your insurance premiums, killing your rental applications, or surfacing as red flags on employment background checks — without you ever knowing why a decision went against you.

If you spot records clearly belonging to someone else but tied to your name or Social Security number, your identity has likely been compromised. Freeze your credit immediately at all three bureaus, file a report at IdentityTheft.gov, and submit a fraud dispute with LexisNexis in writing.

Why this matters even more in 2026

LexisNexis confirmed a data breach in March 2026 exposing 3.9 million records — their second breach in two years. If your file was in that dataset, freeze your credit report at all three bureaus today and pull your LexisNexis disclosure to see what they had on you. The freeze costs nothing, and it converts a stolen SSN from a six-figure liability into a non-event.

How do I freeze my child’s credit report?

Direct answer: Each of the three bureaus lets parents and legal guardians create and freeze a credit file for a minor. The process requires proof of guardianship (birth certificate plus your ID) and is free at all three bureaus.

Children are the highest-value targets for identity thieves. Their Social Security numbers are clean, they have no existing accounts that would raise a flag, and nobody pulls their credit until they turn 18. By the time a college freshman applies for a student loan and discovers $40,000 in fraudulent debt, the trail can be almost a decade cold.

Equifax, Experian, and TransUnion each have a parent-or-guardian credit freeze process for minors. The bureaus typically require:

- A copy of the child’s birth certificate

- A copy of the child’s Social Security card

- A copy of your government-issued ID

- A copy of a document proving guardianship if you’re not the parent listed on the birth certificate

The bureaus process the minor freeze within a few business days. When the child turns 18, they can lift the freeze themselves using the credentials you set up — or you can hand off the PINs and credentials as part of “the adulting starter pack.” The FTC’s guide to protecting your child from identity theft is the best official resource on this topic and is worth bookmarking.

What did I learn from freezing (and thawing) my own credit?

Direct answer: I froze my credit at all three bureaus in February 2022 after Kohl’s called me about an application I never made. I have thawed it three times since for legitimate pulls. Equifax thawed instantly. Experian’s PIN flow was painful. TransUnion was the most reliable. Cost: $0.

The Kohl’s phone call that pushed me over the edge

I work in security for a living, but I still avoided freezing my credit for years because I assumed it would be a hassle every time I wanted to apply for something. That changed the afternoon Kohl’s Department Store called me to say they could not approve “my” application for a store credit card. I had never applied. Someone had enough of my information — name, date of birth, Social Security number, address — to get to the final approval step at a national retailer. They were one merchant decision away from walking out with merchandise on a card opened in my name.

I hung up, opened my laptop, and ran through the exact steps in this guide. I froze my credit at Equifax, Experian, and TransUnion, pulled my LexisNexis report, and enrolled in the IRS’s Identity Protection PIN (IP PIN) program so a thief couldn’t file a fraudulent tax return under my Social Security number. Total time from the Kohl’s call to “everything is locked”: about 35 minutes. I have not had a single fraud incident since, and the entire stack cost me nothing.

The 2017 Equifax breach that exposed 147 million Americans’ data was almost certainly the source of whatever the Kohl’s applicant was using. That’s the lesson: by the time you get the courtesy call, the data is already in the wild. The freeze is what makes the data useless.

A few things I did not expect:

- Equifax’s identity-verification questions were oddly hard. They asked about a mortgage balance from 2015 that I had to dig up an old PDF to confirm. I failed the first attempt, retried with my records open, and passed on the second.

- Experian’s PIN system is the most annoying of the three. When I lost track of my original PIN before a mortgage refinance in 2024, Experian made me mail in a notarized form to regenerate it. That took 12 days. I now store the Experian PIN in 1Password with a calendar reminder to rotate it annually.

- Thawing for a single car loan is faster than thawing for “a few days.” When I bought a car in 2023, the dealer told me which bureau they’d pull (TransUnion) and I thawed that one for 24 hours from my phone in the parking lot. Took under 60 seconds.

- Nobody has ever asked me to thaw all three. In four years and three credit pulls (mortgage refi, car loan, business credit card), every lender pulled exactly one bureau. A targeted thaw at the right bureau is almost always enough.

- My LexisNexis report was 31 pages. When I requested it in early 2026, I found two old addresses I’d never lived at and one professional license that wasn’t mine. I disputed both. The license was removed within three weeks; the address records are still under investigation.

If you want a real-world benchmark, freezing all three credit bureaus, pulling LexisNexis, and freezing my kid’s credit took me one Saturday morning with coffee. It’s the highest-ROI 90 minutes I’ve ever spent on personal security.

Should I lock my credit right now?

Direct answer: Yes. Freeze your credit at Equifax, Experian, and TransUnion today (15 minutes, free). Request your LexisNexis Consumer Disclosure Report (5 minutes, free). Freeze your kids’ credit too. It is the cheapest, most effective identity-theft defense available.

If you take one action after reading this, lock my credit at all three bureaus right now. The credit freeze is free, it doesn’t affect your credit score, it doesn’t break any of your existing accounts, and it stops the single most common form of identity theft cold.

Then layer the rest:

- Pull your LexisNexis Consumer Disclosure Report and dispute anything wrong with it

- Pull all three credit reports for free at AnnualCreditReport.com and review them line by line

- Freeze your spouse’s credit (and request their LexisNexis report)

- Freeze your kids’ credit — it’s the step almost nobody takes, and it’s the highest-leverage move for a child’s future financial life

- Save every PIN and login in a password manager (1Password, Bitwarden, Dashlane, or your platform’s built-in vault) so you can thaw quickly when needed

- Enroll in the IRS Identity Protection PIN (IP PIN) so nobody can file a fraudulent return under your SSN

- Set a calendar reminder to re-check your LexisNexis report once a year, and follow NIST SP 800-63A identity-proofing guidance when verifying new accounts

Don’t wait for a breach notification to do this. The thieves already have your data — multiple times over, between Equifax 2017, T-Mobile 2021, National Public Data 2024, and LexisNexis 2026. The only question is whether you’ve put up the lock.

Update: Just days after we published this guide, LexisNexis confirmed a data breach exposing 3.9 million records — their second breach in two years. If you haven’t frozen your credit yet, the urgency just went up.